Some links may be affiliate links. As an Amazon Associate, I earn from qualifying purchases. This post may include AI-assisted content.

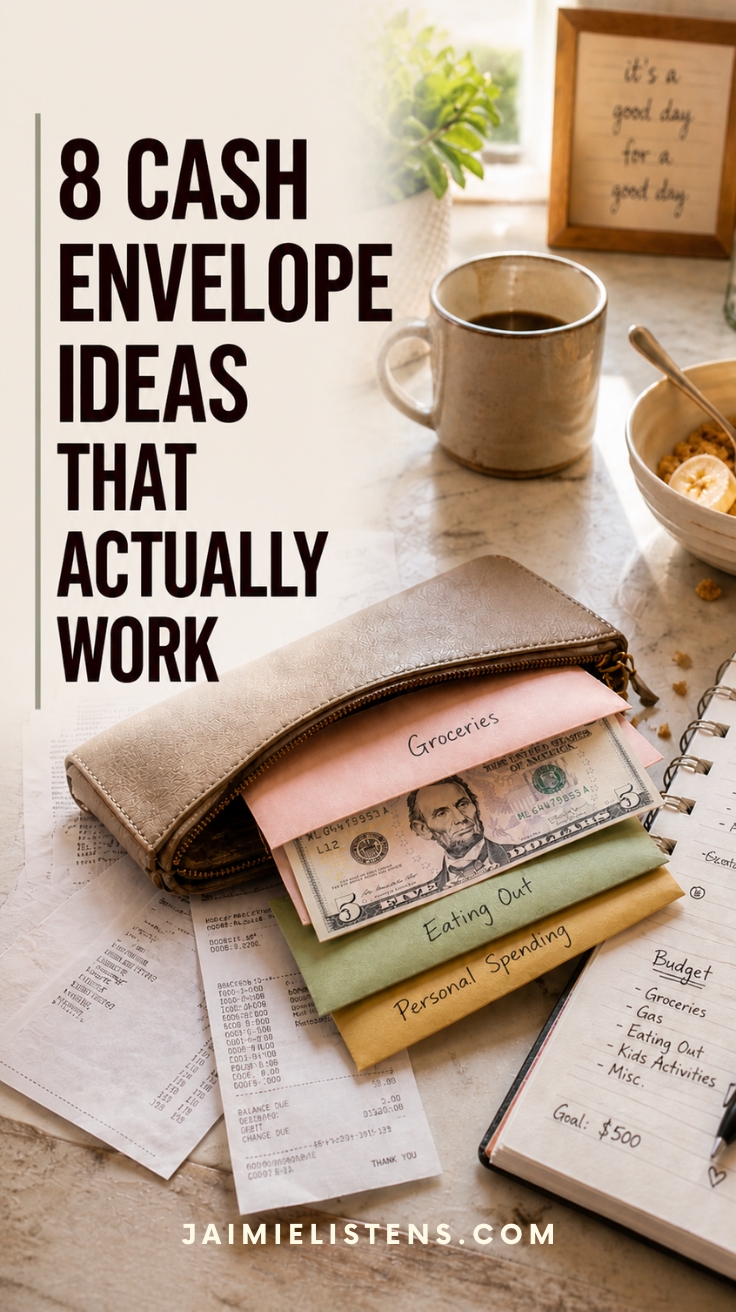

The cash envelope system sounds simple enough when you first hear it: put cash in envelopes, give each envelope a job, and stop spending when the money is gone.

In theory, that makes perfect sense.

In real life, it can get messy fast.

Groceries cost more than you expected, gas jumps again, somebody needs school supplies or work pants or allergy medicine, and suddenly the envelope that was supposed to last all month is looking at you like, “Good luck, friend.”

That does not automatically mean you failed at budgeting.

It may just mean the system needs to fit your actual life instead of some imaginary month where prices behave, schedules stay predictable, and nobody needs anything weird on a Tuesday.

The cash envelope system can still be useful, especially if you like the idea of giving your money clear boundaries (similar to Dave Ramsey), before you spend it. But for a lot of households, it works better when you treat it as a flexible spending-control tool instead of a rigid pass-or-fail test.

You do not have to use cash for every category. You do not have to make 27 envelopes. And you definitely do not have to restart your whole budget every time real life barges in wearing muddy boots.

These cash envelope system ideas are meant to help you use the method in a way that is practical, visible, and realistic for everyday life.

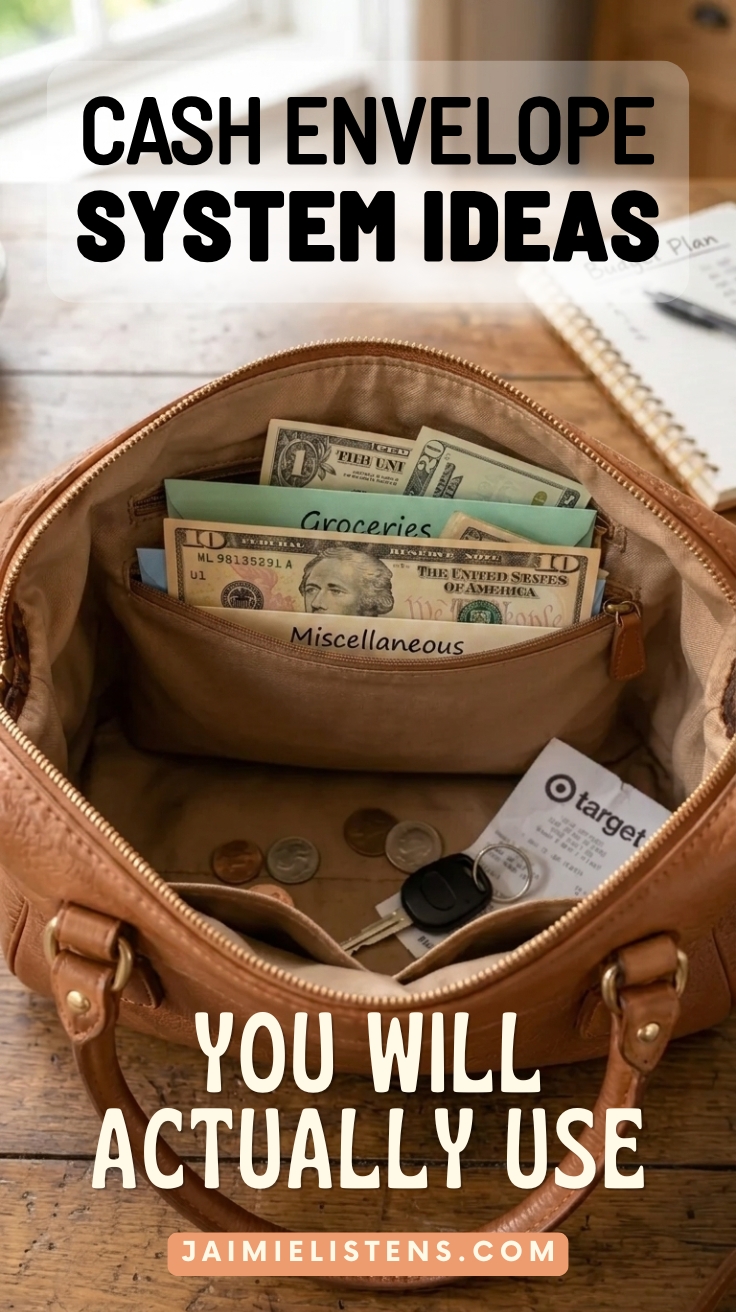

What the Cash Envelope System Looks Like in Real Life

The “perfect” version of the cash envelope system usually looks very neat and tidy online. Every envelope has a label, every dollar has a plan, and everyone involved apparently remembers to bring the correct envelope to the correct store every single time.

Precious.

In real life, the cash envelope system is usually a little less polished and a lot more useful when you stop trying to make it perfect.

It might look like using cash for groceries because that is the category that keeps creeping up. Or, it could mean having one envelope for eating out because takeout is where your budget keeps quietly leaking. It might mean keeping a small buffer envelope because you already know something unexpected is going to happen, even if you do not know what yet.

The point is not to make your budget look impressive on the kitchen table.

The point is to give yourself a simple way to see what is left before you spend it.

That is where cash envelopes can help. They create a physical boundary around categories that tend to get fuzzy when everything runs through a debit card. When the grocery envelope is getting thin, you can see it. Then, when the fun money is gone, you know it. When you keep borrowing from one envelope to cover another, that tells you something too.

That information matters.

Not because you need another reason to feel bad about money, but because a budget cannot help you adjust if it is hiding the truth from you.

So instead of asking whether you are doing the cash envelope system “the right way,” ask a better question:

Is this helping me make better spending decisions in my real life?

That is the version worth building.

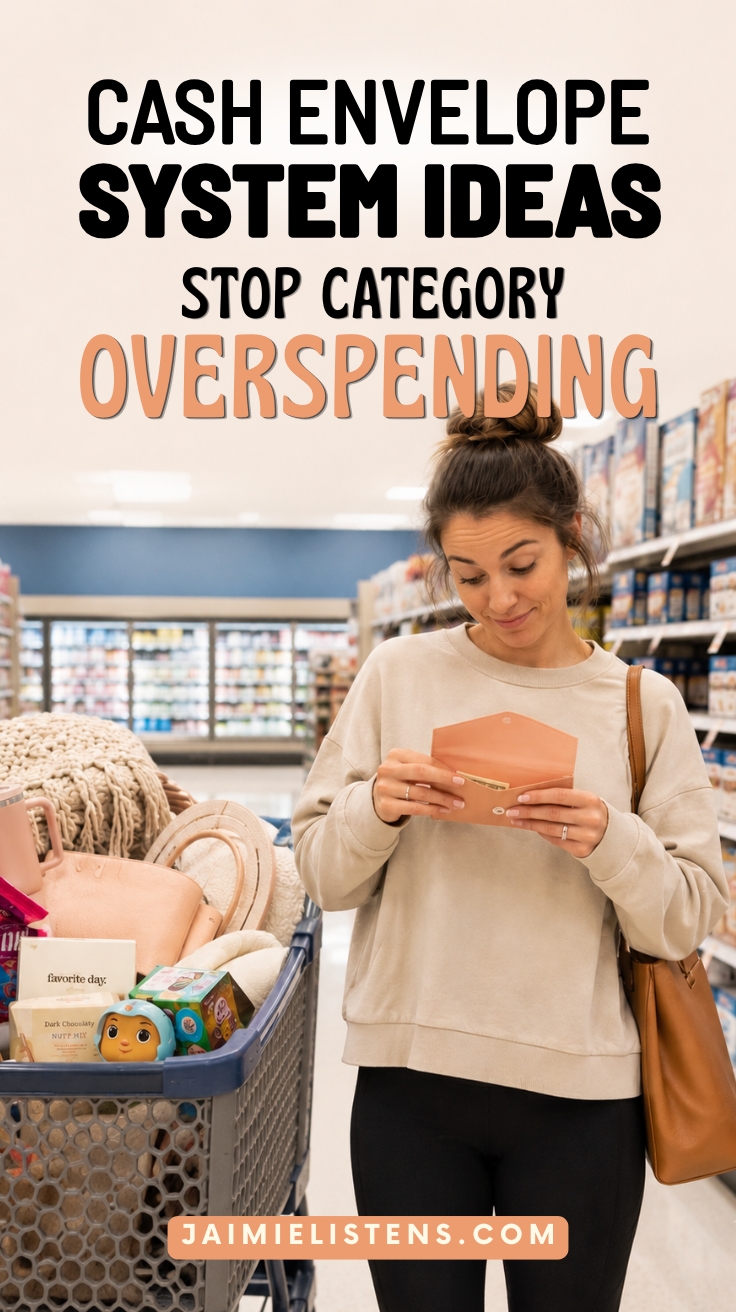

#1 Use Cash Envelopes for the Categories That Actually Overspend

One of the fastest ways to burn out on the cash envelope system is trying to use it for everything.

Every category, every dollar, and every situation.

That sounds disciplined, but in real life, it turns into a juggling act you don’t actually need.

Not every category causes problems.

Your mortgage isn’t randomly doubling mid-month. Your insurance premium isn’t quietly creeping up because you walked into Target for toothpaste and walked out with a candle, a blanket, and a “this felt necessary” purchase.

Cash envelopes work best where spending tends to drift.

That usually looks like:

- groceries

- eating out

- personal spending

- kids’ extras

- anything that feels small in the moment but adds up fast

Those are the categories where it’s easy to lose track because there’s no clear stopping point. Swiping a card doesn’t feel like anything until you look back later and realize how much actually went out.

Cash changes that.

It slows you down just enough to notice what you’re doing without turning every purchase into a whole internal debate. And it gives you a visible limit without needing to check your bank app every five minutes.

#2 Don’t Try to Use Cash for Everything

Forcing cash into every single category is where people quietly give up on this system.

It sounds like discipline on paper, but in real life it turns into friction. Online bills, subscriptions, gas stations that want a card at the pump, ordering anything ahead of time—you end up working around your own system just to function like a normal person.

That’s not a budgeting win.

Cash works best when it’s used strategically, not everywhere.

There are entire categories where cash doesn’t add much value, like fixed bills, subscriptions, automatic payments, and expenses that are already predictable. Trying to force those into envelopes just creates extra steps without giving you better awareness or control.

Where cash actually helps is in the moment.

Standing in a store, deciding whether to add one more thing to your cart, choosing between takeout or cooking at home—those are the decisions that tend to drift. That’s where a physical limit slows you down just enough to notice what you’re doing, without turning it into a whole internal debate.

So instead of asking, “How do I make everything fit into cash?”

Ask a better question: “Where would cash actually help me make better decisions?”

#3 Build a “Buffer Envelope” for Real-Life Surprises

One of the biggest reasons the cash envelope system falls apart isn’t overspending.

It’s interruption.

Something comes up that wasn’t planned for—or wasn’t planned enough—and suddenly you’re pulling from three different envelopes, trying to patch things together and promising yourself you’ll “fix it later.”

That’s usually the moment the system starts to feel like it’s failing you.

But the problem isn’t the system.

It’s that real life doesn’t stay inside neat category lines.

A buffer envelope fixes that.

This is not a free-for-all spending category. It’s a small, intentional cushion that exists for the things that don’t fit cleanly anywhere else:

- a price jump you didn’t expect

- a last-minute school expense

- something breaking, running out, or needing replaced sooner than planned

- the kind of random Tuesday expense that shows up uninvited

Instead of scrambling or borrowing from everything, you have one place to pull from on purpose.

And that changes how the whole system feels.

You’re not constantly reacting. You’ve already made room for the fact that things will come up.

That’s the difference between a system that looks good on paper and one that actually works in a real household.

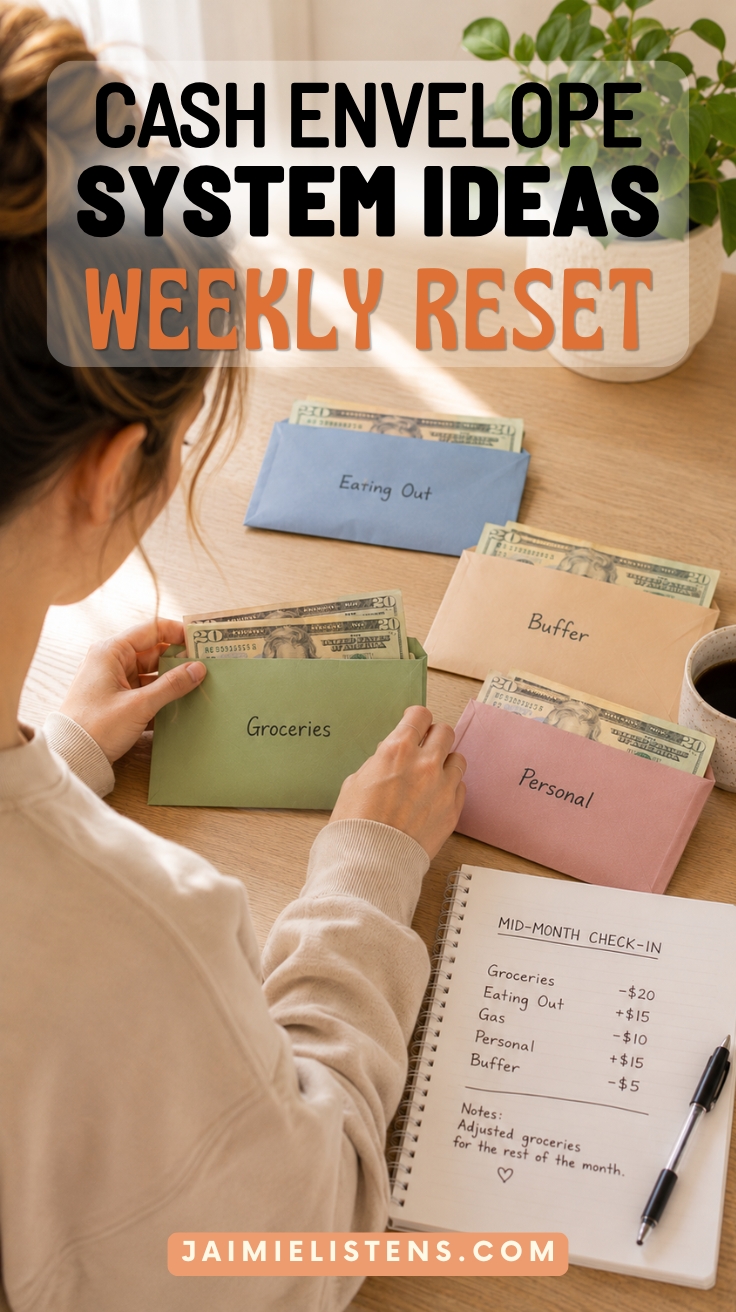

#4 Reset Your Envelopes Weekly, Not Just Monthly

A monthly reset sounds clean and organized.

In real life, it can feel like you’re just… hoping things last.

You set your envelopes at the beginning of the month, and then you’re stuck trying to stretch them across four or five weeks while everything around you keeps changing.

That’s a long time to go without adjusting anything.

A weekly reset gives you more control without making things complicated.

Instead of waiting until the end of the month to realize something didn’t work, you’re checking in while there’s still time to do something about it.

That might look like:

- noticing groceries are running higher than expected

- seeing that one category barely got used

- realizing something needs a little more or a little less next week

You’re not starting over every week.

You’re just making small corrections before things drift too far off.

This is especially helpful if your income isn’t perfectly steady or if your expenses tend to bunch up in weird ways throughout the month.

It turns the system from something rigid into something responsive.

And that’s where it starts to feel useful instead of frustrating.

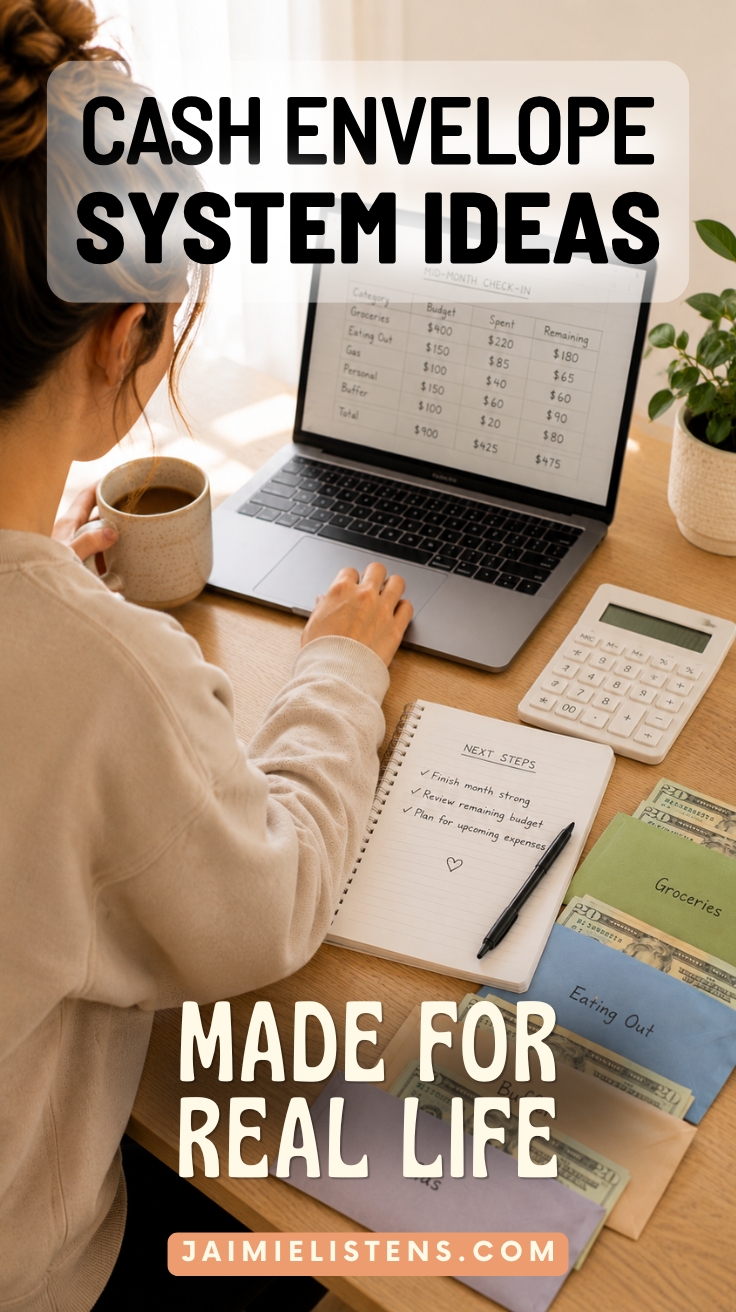

#5 Combine Cash Envelopes with a Simple Tracker

Cash gives you visibility in the moment.

But it doesn’t always give you the full picture over time.

You can see what’s left in an envelope, which is helpful, but it doesn’t always tell you where things went or why one category keeps running out faster than expected.

That’s where a simple tracker comes in.

Not a complicated spreadsheet. Not something you have to maintain perfectly.

Just a basic way to notice patterns.

That might look like:

- jotting down larger purchases

- keeping a running total for certain categories

- or even just making a quick note when something feels higher than usual

You’re not trying to track every penny.

You’re trying to catch trends early enough to adjust.

Because sometimes the issue isn’t overspending—it’s underestimating.

Groceries cost more now.

Certain “small” expenses aren’t small anymore.

Things that used to fit easily in your budget just… don’t.

A tracker helps you see that without guessing.

And when you pair that with cash, you get both sides of the system:

- cash = real-time awareness

- tracker = bigger picture clarity

That combination is what actually helps you make better decisions going forward.

#6 Use Smaller Bills to Make Your Cash Last Longer

This sounds almost too basic to matter, but it changes how you spend more than you’d expect.

When your envelopes are full of twenties, everything starts to feel like a twenty-dollar decision.

It’s easy to hand one over without thinking too much about it. And once it’s gone, it’s gone.

Smaller bills slow that down.

They make spending feel a little more real without making it stressful. You’re not just peeling off one bill and moving on—you’re actually seeing the money leave in smaller pieces.

That small pause is often enough to make you think twice in a good way.

It also helps your envelopes stretch further throughout the week.

Breaking a $20 into smaller purchases feels different than watching one or two large bills disappear early on. It gives you more flexibility and more awareness at the same time.

This isn’t about restricting yourself.

It’s about making your spending visible in a way that naturally helps you pace it.

If you’ve ever felt like your envelope disappeared faster than it should have, this is an easy adjustment that can help without changing anything else about your system.

#7 Keep Your Envelopes Where You Actually Use Them

A system you don’t have with you doesn’t help you.

This is one of those small things that quietly breaks the cash envelope system. You set everything up, organize it nicely, and then… leave it at home.

So when you’re out running errands or picking something up on the way home, you end up using your card “just this once,” and now your envelopes and your actual spending are out of sync.

It’s not a discipline issue.

It’s a setup issue.

Your envelopes need to live where your decisions happen.

For most people, that means in your wallet, your purse, or even a small grab-and-go pouch that comes with you when you leave the house. Not sitting neatly on the counter looking organized but completely disconnected from real spending.

If you don’t like carrying a lot, you don’t need every category with you.

Just bring the ones you’re likely to use that day.

That one change makes the system usable instead of theoretical.

You don’t have to remember it. You don’t have to work around it. It’s just there when you need it.

And that’s usually the difference between something you try for a week and something you actually stick with.

#8 Adjust Your Envelopes Mid-Month Without Starting Over

This is where a lot of people quietly give up on the cash envelope system.

Something goes off plan. Groceries run higher than expected, one category gets drained too fast, or an expense pops up that you didn’t see coming. Then it starts to feel like the whole system is broken, and the instinct is to scrap it and “start fresh next month.”

I get the appeal. A fresh start sounds clean and tidy.

But real life does not reset on the first of the month, so your budget needs permission to adjust before then too.

Moving money around mid-month is not failure. It’s maintenance.

You may shift a little from eating out to groceries because food prices were higher than expected. Another idea is to pause personal spending for a week because the car needed something. You may realize one envelope had too much and another didn’t have enough.

That is not you ruining the system.

That is you paying attention and responding like a grown woman with actual responsibilities and a functioning brain.

A budget is supposed to help you make decisions based on what is really happening. It is not supposed to shame you for adjusting when the original plan was off. You do not have to throw the whole thing away. Simply make the next right move with the information you have.

You Don’t Need a Perfect System — You Need One You’ll Actually Use

The cash envelope system can work, but not if you treat it like a personality test you either pass or fail.

Most people do not struggle with budgeting because they need more guilt. They struggle because life is expensive, schedules are full, prices change, kids need things, cars act up, and somehow there is always one more “small” expense trying to sneak into the week.

A useful system has to make room for that.

The goal is not to create the prettiest set of envelopes or follow some rigid “perfect” method. The goal is to build a simple structure that helps you see what’s left, notice where money is going, and make better decisions before the month gets away from you.

That’s it.

If your envelopes are a little messy, if you only use cash for a few categories, or if you move money around sometimes—that doesn’t mean you’re bad at budgeting. It means you’re adapting the system to fit your household.

And honestly, that’s the version worth keeping.

Start small. Pick one or two categories that tend to get out of hand, set up envelopes for those, and watch what happens. You don’t need a full budget makeover to learn something useful.

If you’ve tried cash envelopes before and they didn’t stick, I’d love to know where it broke down for you. That’s usually where the best adjustments begin.

AI Disclosure: This post was created with the assistance of AI tools for brainstorming, editing, and organization, which helps me manage chronic pain and physical limitations during long writing sessions. All content is based on my real-life experience and is reviewed and edited by me. Some or all images in this post may be AI-generated for illustration and inspiration. Learn more about how I use AI here.

Disclaimer: Jaimie is not the great and powerful Wizard of Oz, a lawyer, a doctor, a veterinarian, or a CPA. Nothing you read in my blog is a substitute for professional advice and doing your own good research. Remember that just because someone has credentials doesn’t guarantee their advice is golden or perfect. Put your smart hat on and do your due diligence. Good luck!

Leave a Reply